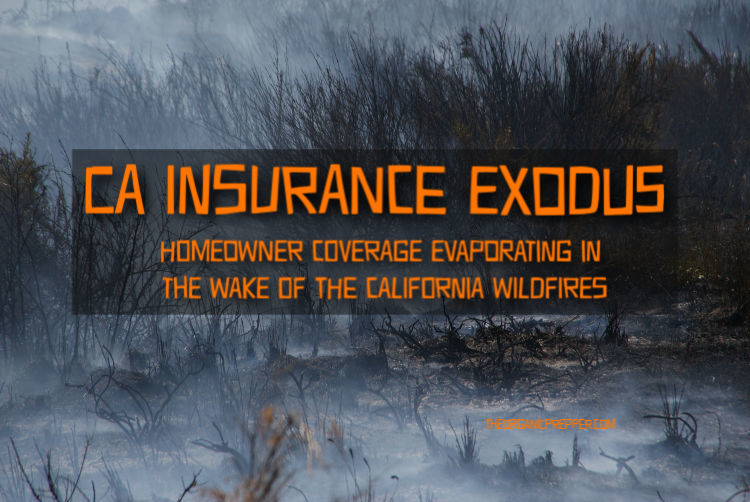

The California wildfire catastrophe continues for many residents even after the fires go out. Vulnerable residents are left with a mess to clean up or their homes have been reduced to ashes.

But even as the ashes are settling, residents of wildfire-ravaged areas that the California Department of Insurance is calling “The Wildland-Urban Interface” or WUI, are facing yet another looming threat. National big-name insurance companies offering home and property insurance are cutting their losses and evacuating California in droves, leaving entire communities in financial crisis.

California communities, already devastated by wildfires or even just in high-risk fire zones, are facing double and triple rate hikes or being dropped from their insurance carriers altogether, reports The Sacramento Bee:

Two consecutive disastrous wildfire seasons have created a budding insurance crisis for thousands of Californians who live in and around fire-prone areas. Stung by $24 billion in losses, insurers are imposing rate hikes or dumping customers altogether, leaving homeowners to seek replacement policies that can be two or three times as expensive. (source)

The rate of affected California residents continues to grow – so far, insurers have dropped 350,000 California residents from their policies.

Insurance companies are leaving California over massive losses.

As Fox Business explains, “Last year’s Camp Fire, the deadliest and most destructive in California history, engulfed more than 18,000 structures and killed more than 80 people before it was contained. It caused more than $12 billion in insured losses.”

Insurance providers face devastating losses from payouts due to wildfires. Some providers didn’t survive at all. One smaller insurer crumbled under the pressure and became yet another casualty of the wildfires. “The Camp Fire…also claimed one additional victim: Merced Property & Casualty, a small carrier that folded under the weight of roughly $100 million in claims from the Paradise disaster,” The Sacramento Bee reported.

Subscribe to our newsletter

Trying to figure out how to stock up while prices keep climbing? We can help with our free guide and newsletter!

Other insurers are taking note of the demise of one of their own and are getting out of California’s high-risk areas. This poses a massive problem for the residents of those areas, many of whom are low-income families without the resources to endure sudden enormous increases to their insurance premiums even while state officials struggle to enact insurance reform.

Insurance Commissioner Ricardo Lara favors a proposal by the legislative task force to create state subsidies for those living inside the fire zones, which tend to be people who are already struggling economically. “There’s this misconception about folks living in the (fire areas), especially in Southern California — people think there are these multimillion-dollar homes in Malibu,” he told The Bee.

Many long-time residents are scrambling to find affordable home owner’s insurance after either receiving notice of cancellation of their policy or enormous rate hikes. Those with existing mortgages are required to keep insurance in order to keep their homes. Their options are either to find an insurer or be forced to sell their home. Some who have paid off their homes are simply risking being without coverage.

Penny, a real estate agent who shared her story with The Organic Prepper, said: “They can no longer afford their mortgage they were able to qualify for AND the additional insurance payments. And if you don’t find insurance, your lender/bank/mortgagor will tack onto your payment to cover the insurance thru (sic) some affiliate they have and you loose (sic) the option to shop for something affordable. Those who have their homes paid off are opting to not cover and figure they will just have a mortgage if a fire occurs. Some have lowered it by raising their deductible.”

“It’s really sticker shock for people to see their homeowners’ (premium) go from $1,200 to $3,600,” The Bee reported.

Residents don’t have many options to turn to.

As insurance rates rise, customers are looking desperately at every option. But there’s not much to choose from.

Some residents are forced to turn to insurers of last resort when even insurers like Lloyds of London, who are known for their high-risk tolerance, deny coverage. Those options are limited, expensive, and disappointing.

Penny told The Organic Prepper that “It came up in the public meeting that I believe Lloyd’s of London was one of the few writing policies for a bit and suddenly the light came on what a risky area this was considered and they sent out cancelation (sic) notices in mass giving 30-45 day notices to find other insurance.”

The last resort after homeowners have exhausted all other options is an expensive, short-term band-aid called FAIR, as The Bee explains:

If all else fails, they go to the California FAIR Plan. The FAIR Plan, created by the California Legislature when insurers abandoned inner cities following the 1960s riots, offers bare-bones coverage that doesn’t include theft or liability insurance. It isn’t subsidized by the state. FAIR Plan rates are regulated, but with fewer limitations compared to the traditional insurers. (source)

“The California Fair (sic) Plan is considered the wrap around plan covering the structure in case of a fire and your other insurance will then cover the contents,” Penny told us. This means that the FAIR plan will only cover your structure, and the owner will have to get additional insurance to cover anything else including contents. Penny continued, “The California Fair plan, it was made clear in the meeting, is not a long term solution and for many, it’s not an affordable option.”

Some homeowners got creative with finding obscure insurance loopholes like Lynda, who shared her story with The Organic Prepper:

“We have lost 4 insurance carriers in 3 years because of our wildfire danger. We have never filed a claim… We have insurance through the farm bureau now through a company called The Grange because we have livestock…we found our best option was to insure as a farm, which we meet the criteria for, even though it’s considered a hobby farm. The insurance was lower too.”

Insurance companies are using questionable methods to evaluate risk.

Insurance companies are dropping their customers or raising rates because of the location of the homes, even if the homeowners take it upon themselves to install elaborate “hardening” systems to protect their homes from fires.

The Bee reported a story on Jennifer Burt, a local CA real estate agent:

…she’s done everything she can to fire-proof her home in Meadow Vista, in the bushy, densely wooded Placer County foothills, even installing a sprinkler system on the roof. Yet a few weeks ago, her insurance carrier — Lloyd’s of London, known for insuring high-risk properties — told her it was declining to renew her homeowners’ policy. (source)

Insurers don’t even visit the property to see what “hardening” has been done. They lump the “bad” with the “good” risks by area and leave responsible home-owners in the lurch. Penny told The Organic Prepper she is concerned about this method of determining coverage and premiums:

“What we are seeing is that the insurance companies are not coming out to the location of the home, but looking at the location on a satellite map and declining without ever driving by or stepping foot on the property.

Many companies are looking at the chances of a particular area in general and the likelihood of it going up in flames. They then look at the ratio of houses they currently insured in that area and if it did go up in flames, what is their loss % ratio and could the company survive a hit like that. At least one company went under the Paradise fire which is the basis of their findings. Other companies just say no. Not risking it.”

It’s a problem that the California Department of Insurance takes note of in their report titled The Availability and Affordability of Coverage for Wildfire Loss in Residential Property Insurance in the Wildland-Urban Interface and Other High-Risk Areas of California: CDI Summary and Proposed Solutions:

Based upon complaints received from homeowners and members of the Legislature, the majority of non-renewals, refusals to insure, and increased premiums in these rural areas were the result of insurers’ greater use and emphasis on wildfire-risk models, which are used to underwrite and rate residential properties. Legislators, other public officials, and their constituents have expressed concern that wildfire-risk models are not accurate, do not provide satellite imagery that is granular enough to objectively identify fuel sources and other physical characteristics, and do not take into account mitigation done by the homeowner or the community. Since the wildfire-risk tools that insurers use have a measure of objectivity and a relationship to the risk of loss, CDI lacks the statutory authority under current law to prohibit an insurer from using these tools to determine whether it will issue or renew a homeowners’ insurance policy. While CDI has authority over how an insurer uses a wildfire-risk tool to classify and rate individual properties in a homeowners’ insurance program, we have no authority over the development and construction of the models. (source)

Leaving the area is not always a viable option, either.

Some find it impossible to find an affordable option and are forced to sell. But cutting their losses and getting out is still expensive and hard to do. Many are facing plummeting housing prices.

Penny told The Organic Prepper what some of her clients are experiencing:

“As a realtor, I had a full price offer in Sierra Springs last May and buyers backed out because of the cost of insurance. Another listing, we came down $65k to try to get an offer. They finally got one after lowering it a total of $120k. The original price was a good, mid grade price for the property.

And yes, buyers were discouraged due to the cost of insurance. What would have cost roughly $750 a year to cover, is now costing $3,800-$6,800. These were the bids we were receiving. The best quote at $3,800 was thru USAA which is available for vets, but not the general public.

It is so bad, as listing agents and buying agents, we are bending over backwards to find quotes before going any further. But, I have also heard of the current company covering the home, somehow finding out that someone is inquiring about insurance quotes and then dropping their coverage. So, we have to tread lightly as agents when we are trying to get quotes prior to a sale.

It’s a serious problem that we are trying not to panic about, but it is affecting us as we live here too.

Higher-end homes in the Pollock Pines area are getting quoted much higher.

I heard from another agent, his client’s home was 3,500 sqft and their insurance was being dropped. The lowest quote he could get was $20,000 a year. So, now, he can’t afford to keep the home if he wanted to, and no buyer would be willing to step in at that price. I’m afraid that we could see a market crash as the problem isn’t being fixed.

So, the result is that even tho prices are good and getting better for buyers, after tacking on the inflated insurance payment, buyers now can’t qualify for the mortgage payment they could have and they are having to lower their standards across the board to find something they CAN afford.

It is killing the market. The only ones able to afford are coming from the Bay Area.”

Penny is not the only one who fears an economic toll on the real estate market in the fire-prone areas of their state.

Jennifer Burt’s story from The Bee relayed the same fears: “I get so frustrated that the insurance commissioner won’t do anything. It’s reaching a point where it’s a daily conversation in my office as to whether insurance rates are going to kill real estate in California.”

What do you think?

The wildfires continue to have long-reaching consequences for California residents that include economic hardships and a looming real estate market crash due to astronomical insurance pricing. Have you experienced hardships due to rate increases or being dropped by an insurance carrier? What issues are you facing regarding the increased prices for California home and property insurance?

About Jenny Jayne

Jenny Jayne is the mother of two wonderful boys on the Autism spectrum and is passionate about Autism Advocacy. She is a novelist who writes Post-apocalyptic fiction and a freelance writer. Her first novel is coming soon to Kindle eBooks near you. Her guilty pleasures are preparing for hurricanes, drinking hot coffee, eating milk chocolate, reading romances, and watching The Office for the 50th time. Her website: https://jennyjayneauthor.wordpress.com/

54 Responses

Unfortunately what is going to occur in CA. is,people living in the high fire prone areas will end up cutting their losses,walk away from their houses,and leave CA. for lower cost states and start over.Millions of middle class Californians have already sold their houses because of the high cost of living across the board and moved to lower cost states across the U.S.,and are now living like royalty.Eventually,CA. is going to lose a vast majority of it’s tax paying citizens in the near future.This in turn will collapse the CA. economy.Most of the wildfires that are occurring could have been curbed if it hadn’t been for the lack of action by the state government.These fires are the result of 40 years of forest and wild land mismanagement.No logging,no clearing of the forest floor of any debris,no controlled burns,no nothing.The state government let the land grow wild.Now they are seeing the results of their lack of forest and wild land management and everyone in CA. is paying the price.

Same thing is happening/has happened here in Florida. We were customers of MET for over twenty years, both in Florida and another state. When we moved back here ( N/C Florida) they would not cover our new home. Nor would State Farm or Allstate.

In 2004 Florida experienced 3 major hurricanes within 3 months. The larger Florida insurance companies bailed and left folks to pay their own bills. This of course killed the housing market and the snowbirds walked away. With only a few insurance companies left, Florida government decided to create a state run housing insurance group. Then they increased all property taxes by 50% for every home owner in the state, whether your property was on the coast (beach) or not. They negotiated with a few insurance companies to stay and underwrite policies but of course those policies doubled in cost. One catch was to be insured you had to have a mortgage; if you owned your home free and clear, you could not get insurance unless you paid the entire year in advance. After about 10 years, the rates began to level off, but all homeowners are still paying for the #$@! people who build near the coast or on the beach.

I feel sorry for the people who own property in California. At this point things are so bad I don’t know if it is even possible to fix the problems in their state government. But believe me when I say that it is going to cost all of us; national insurers will raise the rates on every policy no matter where the location.

Americans nation wide are already paying for insurance losses in other places and states, with suttle raises in rates. We all pay for a loss anywhere. I dare to name any Insurance company that does’nt do it, HOUAH

Insurance rates are based on the loss ratio for the state. I do not pay for CA, FL, or TX losses. My tax dollars continue to pay to rebuild/repair in TX and FL but my homeowner rates do not.

Insurance companies are going to force the feds and states to deal with climate change and firearms. No homeowners insurance will have kneecap the banks and investment market. Won’t come a day too soon in my book.

That’s an astute observation and a concerning one. Rates across the nation will rise for everyone.

Very good article. No, I’m not her dad.

Thanks so much, Cliff! Feel free to check out my website and other articles here on The Organic Prepper. Thank you for reading. Much appreciated.

Perhaps it is necessary to build a home that will not be damaged by fire. If someones home has been destroyed by fire in a fire prone area, it would be logical to do this

One such type of home is described on the website http://www.monolithic.com.

It is classified by fema as near absolute resistant to natural causes.

Its also resistant to earthquakes. Spend some time browsing the site to get a complete picture of the structure. They have some good home plans.

Have you looked into David South’s monolithic domes? It is rated at Hurricane category 7. I read a story sometime back where a first responder went to this one individuals house to tell them to evacuate. However the responder got caught staying there due to the fire. The waited the fire out. The house was a dome and did not catch fire. Building the same type of house is crazy. Also the domes can be inverted for earth bermed, this saves on heating and cooling. This is what I wished I had done.

I work for an insurance brokerage in CA so I’m seeing this first hand. Our agents are spending all their time trying to keep up, but it’s a game of whack-a-mole with insurance carriers right now. One quote came in Friday for a high-risk area: $44k/yr for a 3,000SF home. I’m building a home out of Insulated Concrete Forms (ICF) in California. My builder is very busy building homes for people in NorCal that lost theirs from fire recently. We need to be building air-tight homes with sealed/conditioned attics. It’s the eve vents that often suck hot embers into the attic, which is a tinder box.

How to get air-tight: Build new homes to “Passive House” standards, use AeroBarrier, the revolutionary new method to seal new build homes. Properly designed Passive House homes also consume just 10-15% the energy of a standard home.

Existing Homes: retrofit with ember-proof vents such as those by Vulcan: https://www.vulcantechnologies.com/

Aero Barrier: https://www.youtube.com/watch?v=XpTdrVESqJg

ICF: Mold, pest, rot, fire, water, hurricane, and bullet proof homes: https://www.youtube.com/watch?v=nY8Hxki7-G0&t=514s

What is Passive House? https://www.youtube.com/watch?v=Hz6qomFM_dw&t=62s

Good for you for building proactive. However, let’s up it a notch. Stainless Steel L Brackets and reinforced sheer walls for earthquake support.

Reinforce all piping going into the home and no plumbing or electric through concrete such as slab.

PVC is a no no in earthquake prone areas. Plastic breaks.. broken sewer lines in walls are nasty.

Lucite over glass.. especially for skylights, and get the thickest made, but be prepared with tarps after a major event..

Security build to foundation beyond building code.. so how about every 6 to 8 inches instead of 16 to 18. Small cost now, but when the ground shakes, your home will not be destroyed.

PVP are always a good idea when brown or blackouts happen

good luck living in the big C Shake n Bake; Fruits and Nuts. California

I can see why the insurance companies are leaving their California customers high and dry, but I can’t imagine how these poor people are going to cope. It seems that California just doesn’t care about its residents as much as the environment. I wonder if residents that have been burned out could file a class action suit against the state for the on-going mismanagement of forested areas that has contributed to the fires, or against PG&E for bad infrastructure.

Not that they will probably get much out of such a suit, and they will probably all die from old age by the time it gets through the courts, but it might be worth trying, if only to hold the responsible parties accountable.

What a mess! I don’t think that I would stay there under these circumstances, and I don’t understand why California doesn’t seem to care about these people.

The bad news is the libs will be invading the rest of the USA. They need to stay there and live with what they created. They are not wanted elsewhere. Their insanity needs to be quaranteened.

Thank you for commenting! Please note that in the article the statistics show that it’s mostly rural communities and low-income families who are being affected most. Many times those are the demographics that include more conservative values.

More unintended consequences when you let environmental leftists run policy in your state. Don’t take out the brush and trees under power lines, and what do you get – fires. Spend money on healthcare for illegal aliens instead of burying power lines going across country, and what do you get – fires. Reroute water to save one little fish, what do you get – drought in your farmland. Shut off the electricity to supposedly prevent fires, and what do you get – SHTF for people who can’t charge their cars, phones, computers, no electric appliances (stoves, washers, radios, heaters, etc), closed banks, closed gas stations, closed stores, closed medical facilities, and so on. Now companies are no longer willing to insure the people because of the political craziness in the state. This is what you get when you vote in leftists with their big ideas on providing everything, but what is actually needed.

It’s truly SHTF for many in CA.

Excellent article and point well made. I will forward extracts-! Beside Marvelous Marin we have a home in Rural Shasta County and our neighbors had already gotten notice of non-renewal. CSAA has been great and last check no plans to change for us. I will explore the aig-ranch option suggested here as well.

For the knowledgeable, capable, well prepared; and of course the “well off” areas outside of our dystopian cities will remain very, very attractive places to live. Other than the fires and earthquakes. LOL

Thanks so much for sharing and thanks for commenting! I’m glad you found the information on insurance helpful in your situation. Many people are looking for more obscure insurance loopholes in order to get coverage. Good luck!

I left CA in 1977. My husband worked for the state forestry department doing local area fire danger assessments that determines where brush or fallen trees had become a fire danger. Then a crew could go in and cut brush or fallen trees and get it out of the Forrest. That practice was stopped later and that has left state residents vulnerable. In fact many other places are in the same danger when Federal forrests are no longer being managed to reduce the fire danger in areas with people living there. Its one thing to let forrests burn in areas where no people live. In areas around towns and resorts with lots of people it can be deadly to neglect cleanup.

That’s a great look at how CA has changed their policies for the worst. Thank you for sharing.

I have been an insurance broker for 30 years and may be able to shed a bit of light from a different angle on this situation. Firstly, it’s helpful to look at the total contract of a homeowner’s insurance policy. God forbid a home should burn to the ground in one of these wildfires the insurance company must pay for reconstruction, replacement of all personal property, and the living expenses for the displaced family while their home is being rebuilt. On a home insured for $300,000 that would include an additional $225,000 for personal property and an additional $60,000 for loss of use; that’s $585,000 that the insurance company must pay for that one loss. If their annual premium is $1000, it would take 585 years for them to break even assuming there are no other losses. (The 18,000 homes lost in the Camp Fires were likely insured for much higher values than these.)

Due to several reasons, but certainly high on the list is the political policy of not allowing the removal of debris to create a defensible space around structures; as a result insurance company’s have become more sophisticated in their underwriting practices. They have “wind maps” and brush calculators that can predict where ash would fall in a wildfire situation. In order for them to be able to pay the claims for clients in sudden and accidental circumstances of loss they need to be at an equal risk factor, otherwise the lower risk more responsible communities have to pay higher rates to subsidize the less responsible higher risk communities.

At the end of the day the insurance company’s have to collect as much in premium as they pay out for losses and their operating expenses or they go out of business. That is why California is losing insurance company participation and having such far reaching financial turmoil.

Thank you for that insight.

As it has been noted in other, various reporting, this is the new normal for CA.

Expect wildfires, rolling multi-day blackouts, and increasing insurance premiums.

I spent 43 years in the business before I retired and you have made a good assessment. I think the real danger will come sometime in the future with this scenario: The state, responding to howls from homeowners/business-owners about the lack or high cost of coverage will do something foolish like attempting to mandate the amount companies can charge or otherwise restrict cancellations or non-renewals. This will create a huge exodus of companies out of California. They will simply give up the California market entirely thus creating a catastrophic crisis in the real estate market and plunge the whole state into recession/depression.

That’s pretty grim, but it seems like that the road they are headed down. They have started instituting rent control. Insurance control seems a “logical” next step.

That’s very interesting. All this billions of dollars in damage goes back to CA forestry not clearing brush. Which goes back to legislation not allowing clearing of brush and trees. Interesting.

Is lack of underground electric lines – not high voltage transmission – also a result of CA legislation?

If the power lines above ground is only electric company decision & their sparked lines/transformers were cause of some fires (in dry areas not cleared of brush), why are there not lawsuits against power companies – by individuals & insurance companies?

There is a pending lawsuit against PG&E

That’s the way it works. And California’s insurance commissioner approved it. You know the guy California; you voted him into office.

This always happens. I’m in Florida, a year ago we were hit by Hurricane Michael. My home was very badly damaged. We had to have structural engineer determine if it needed to be bulldozed or fixed. Lost probably 70 percent of my belongings. I had State Farm and they fixed my home, and didn’t cancel me. My neighbor had less damage, and was covered by ASI (a progressive insurance affiliate) He got cancelled. There is no logic to it. But seems like people have to expect mass cancellations after a huge disaster. Unfair. But to add to the confusion, getting insurance in the first place was very difficult when I bought my older home 5 years ago. So many companies either weren’t writing older homes or weren’t writing at all. Now my home is built to current codes, but can’t find a different company to cover me…I expected state farm to cancel me and was looking…I literally cried from joy when I got my statement for the upcoming year…they didn’t cancel me.

What a relief! It’s so strange how much we depend upon insurance now. Myself included.

More victims of their own making. Decades of liberal agenda driven environmental policies and laws. They all point fingers at everywhere but themselves. It’s always someone else’s fault. You made it you clean it up. Oh yeah you can’t cause now your outnumbered because of other failed socialist laws and policies.

It’s people living in rural areas who are being hit hardest by this; it’s people living in Silicon Valley and LA who are voting in all the nitwits. Rural Californians tend more toward Reagan Republican politics than toward Moonbeam Brown politics. Have some compassion for the folks being denied their right to life, liberty and the pursuit of happiness in the locality of their choice due to Agenda 21/2030 policies.

That is exactly how it work in NY State: the five counties of NYC, plus Albany and Buffalo (Erie Co), control the state politics. The other 55 counties of upstate and rural is Red as a stop light. Just outnumbered.

I know this has been said before, but the true CA voters must change their voting habits by wising up and ridding themselves of their true problem, the Dem. party’s control of of not only the local and state government but their lives. Put some people with common sense and ability to actually lead snd who can get rid of asinine laws and regulations, you can call it MCGA because now there is a good example and pattern to follow.

@Kate: my guess is that there is no longer any point in a non-marxist Californian going to the polls and casting a vote. They are outvoted every time by the Bolsheviks in the urban centers. Just as the city of Chicago controls the state of Illinois, and the island of Manhattan controls the other 4 boroughs of New York City and the entirety of New York State. Voting in such states is pointless. It’s like telling Venezuelans they could have saved their country by voting. Eventually people either vote with their feet or resign themselves to a degraded lifestyle in a “soviet republic.”

Everyone had better keep a close eye on their insurance premiums in the coming months. This disaster is purely a west coast problem, but the insurance co.’s WILL try raising rates on east coast customers to offset their losses…even as they drop coverage for 350,000 customers in CA.

Keep in mind that you can always confront your insurer over this issue. I did this once over a Katrina rate hike and succeeded in having my rate returned to the lower level. Nothing ventured, nothing gained, folks.

Great tip! I’m going to watch my rates closely.

Do not entirely blame PG&E. Remember they are highly regulated and their rates set by the Public Utilities Commission—a state controlled agency. Also do not point to PG&E’s executive pay and bonuses. They have to compete in the CA executive salary market for talent.

Until you (we) get some sanity in Sacramento, CA is only going to get worse.

NO, I do not work for PG&E—never have. I am a retired business owner who suffered 30 years of trying to do business in CA. I should have been a politician, retired with full benefits and a sweet pension. Too honest I guess.

I feel sorry for the people but I am tired of tax payer dollars being feed to areas that rebuild and are destroyed again and MY tax dollars pay to do it again. Fires, hurricanes, tornados and earthquakes happen and happen again in and around the same locations yet we pony up more tax payer money to build, replace and repair to wait for the next disaster to occur. That is INSANITY!

Yeah if possible NEVER BUY INSURANCE!

Their goal is to find a way to deny liability & NOT PAY.

They are the scum of the earth.

It’s a complete rip off.

Oh they’ll happily take your money but when it come to them making a pay out get ready to jump through hoops if fire & end up in a court case that will send you broke before the6 pay a cent.

They totally game the system, willingly destroy innocent people’s lives before they pay out a cent.

Hey, this IS California. Nothing that some higher taxes won’t fix.

Why don’t we shoot ourselves in the other foot while we’re at it? The banks require that you have homeowners insurance in order to carry your mortgage. What happens now when homeowners can’t get insurance — will CA force the banks to continue to carry uninsured properties?

This is all going someplace ugly. The Golden State of California was built on speculation. The Left has a very risky speculation when their bed is too short and their covers too narrow.

Exactly. The law is that you must have home insurance in order to have a mortgage.

There is also a high probability that some of these fires may be beyond the scope of PG&E. All those areas north of the Bay Area and surrounding LA are high geo-thermal activity areas. It wouldn’t take much to spark an area leaking methane gas all over the place. Californians are at the mercy of more than corrupt politicians and corporations. Clear Lake and the area northeast of LA, Tehachipi and out to Death Valley/China Lake — all loaded with geo-thermal activity.

Then, there is also the ten year drought which (supposedly) is a God-thing. It will take many more rainy seasons to fix that disaster.

The new normal: annual wildfires, power outages, and now increasing insurance costs.

They are probably going to have to expand the FAIR plan to include the contents, living expenses as the dwelling is rebuilt.

Wonder what those costs will look like.

All else fails, create a state ran fire insurance/tax plan based off sqft. and home value.

This is just the next step in implementation of Agenda 21, now known as Agenda 2030. It’s the eugenicists’ long-term depopulation plan, by first removing people from rural areas and redesigning mass transit so people cannot travel to rural areas; forcing people into self-driving vehicles is part of that step as well (hello, 5G is here today). Once people are concentrated into urban areas they are much more easily controlled, and culled.

Traitors to the human race who are on the take from the eugenicists will dismiss this as “a conspiracy theory,” but sadly, it’s not theory at all, but rather in full implementation phase. 5G is being rolled out with the government-subsidized goal of forcing people to use only computer-driven vehicles or mass transit (same thing). Insurance rates are exploding to make sure people are unable to afford to live in locations designated by the UN’s Agenda 2030 as off-limits to humans. It’s real, it’s happening even as you read this, and so long as you allow it to continue because you’re afraid of someone sneering at you about being a “conspiracy theorist,” the mass-murdering elitists will continue to arrange carefully-planned deaths for most of us.

I would like to see the literature support this. I’m interested.

At last! The first comment on here from someone who really understands what’s happening. The fires are being started deliberately, and so are the extreme weather events through constant geo-engineering. This is indeed about deliberate rural land clearance and depopulation as part of the Agenda 21/2030 Agenda. Wake up!

This is an Orchestrated event.. Part Agenda 21 (Move to drive people from rural and small town America. Part the elites ongoing efforts to steal the wealth and value of property from America’s middle class..

In big cities it runs on about a 40 year cycle.. You see nice neighborhoods.. working people move in buy homes.. homes appreciate.. Then suddenly criminality which once was fairly unheard of becomes common place. The homeowners now older or retired with much of their wealth in their homes sees that wealth lost as the criminals roam the streets and the elderly homeowners live behind bars.. to keep the intentionally permitted criminals out.. When values plummet Tax payer funded Urban Renewal and the cycle begins again.. While the old folks driven out forced to sell at discount prices .,.. Live in one bedroom studio apartments on Cat food…

It seems our government doesn’t care about this nation and maybe the elite is overpowering them and destroying us. All of the bad things happening are prophesied in God’s word.

Start Personal civil suits against all the so-called lawmakers in Sacramento that write laws prohibiting proper maintenance of the forests. This area has been burning for thousands of years. The burning stopped when the logging industry cut logging roads and fire breaks into the forests, The companies also culled the ddead and diseased trees keeping the forests much more healthy and without the fuel load currently in place.

I have no love for the insurance companies, but they are trying to stay solvent in an extremely business toxic situation. Place the blame where it belongs – on the liberal tree huggers.

Tens of Millions of American households are going to learn the hard way how much their lifestyles have been subsidized or mispriced.

Thinking one can live in the middle of a highly flammable landscape without consequences is hubris.

Thinking that a bankrupt government is going to continue be storing lavish subsidies is foolish.

People should start deep thinking about where they live.

Oct 27, 2019 THE NEW AGENDA 2030 NORMAL

The latest PG&E related fires in California are to be expected if you’ve come to accept that it’s all just part of the new “normal”…

https://youtu.be/rAGpetkg_vw