Author of Be Ready for Anything and Bloom Where You’re Planted online course

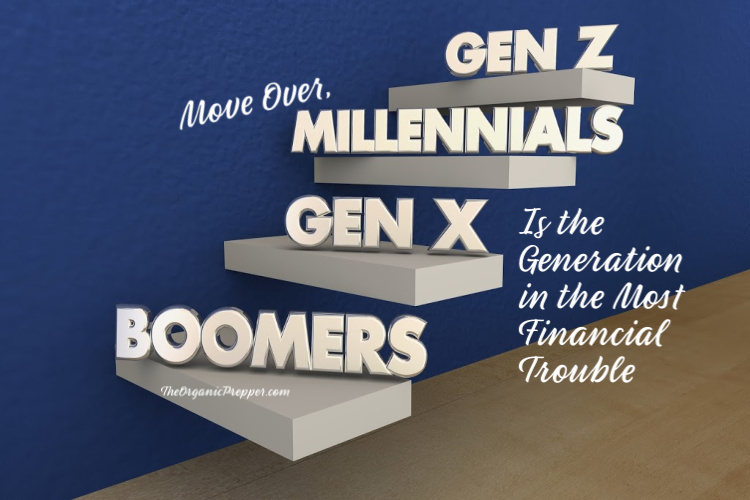

Everyone picks on Millennials these days but a new study by Lending Tree shows that out of all the generations, Gen X is the one dealing with the deepest financial problems.

First, some definitions.

- Gen Z or Centennials: Born 1996 – current day

- Millennials: Born 1977 – 1995.

- Gen X: Born 1965 – 1976.

- Baby Boomers: Born 1946 – 1964.

- The Silent Generation: Born 1945 or before

We all know that two major financial mistakes are getting into debt and failing to have an emergency fund. A recent study looked into the debt levels of each generation.

The study

Lending Tree, an online lending marketplace, did a study on the 3-year changes in each generation’s debt.

As each generation moves into different stages of their personal and economic lives, the amounts and types of debt they carry shifts, too. We compared the debts of members of the four adult generations — millennials, Gen Xers, baby boomers and silents — between March 2016 and March 2019 to see what’s changed.

Specifically, we calculated the changes in the average balance of each major debt category — personal loans, credit cards, auto loans, student loans and mortgages — and the change in the percentage of each generation that carries each type of debt. (source)

Here were the key findings:

- Millennials saw the greatest spike in overall debt. Their total balances rose by an average of $16,714 — almost 29% — between 2016 and 2019.

- Gen Xers now have the highest average debt burden of any generation. They increased their average debt burdens by about 10%, or $11,898, between 2016 and 2019, thanks to steady dollar increases across all debt categories.

- Older generations — boomers and silents — are winding down their debt, thanks to decreases in average mortgage balances. However, they’ve increased their average debt across all other categories.

- Boomers decreased their debt burdens by 7%, or $10,424. Members of the silent generation dropped their overall debt by $9,486, or 8%. (source)

But what about Gen X? Why are they in so much trouble?

Subscribe to our newsletter

Trying to figure out how to stock up while prices keep climbing? We can help with our free guide and newsletter!

Gen X has financial problems in many ways.

Marketwatch did an analysis on that the ways that Gen X is financially wrecked and it’s not pretty. This is my generation so I was especially interested in their analysis.

They’ve got the most credit card debt of anyone — yet still spend more than anyone on non-essentials…Despite their sky high credit card debt, Gen X spends big on non-essentials, according to data released in 2018 from finance site Bankrate.com. Indeed, “Gen Xers (ages 38-53) spend $3,473 annually on restaurant food, prepared beverages and lottery tickets, the most of any generation,” the report reveals.

They’re woefully under-saved for retirement…Median retirement savings for Gen X is only $35,000, the same median amount as millennials, despite Gen Xers being much closer to retirement,” according to a study of 3,000 Americans by Allianz Life. Having just $35,000 in retirement savings — especially when you’re a Gen Xer ages 37- 51 — is not even close to enough. Fidelity recommends that by age 40 you have three times your salary saved for retirement. Gen Xers may be so under-saved thanks to the competing financial demands of children… and caring for aging parents.

Their average debt now tops $150,000. Not only is their credit card debt high, the total amount of debt they have is. Those in the 35-44 age group have “the highest debt levels of any age bracket,” SmartAsset notes, citing Federal Reserve data.

They’re more likely than other generations to say they can’t meet their financial goals. All of this debt and the lack of savings may explain why fewer than 1 in 3 members of Gen X says they think they can reach their long-term financial goals, according to a survey released in 2017 by FICO. (source)

That’s not a pretty picture for people between the ages of 37 and 51.

Some of the reasons for this financial mess

Reading over the data, the thing that jumps out at me is that people of my generation are at the point where they’re taking care of everyone. Some still have kids at home, while others have adult kids who have returned home. We are often lending a helping hand to our adult children who are in college or trying to get their feet on the ground. Some of this generation are taking care of aging parents.

It’s pretty tough to save for retirement when you have all these people depending on you.

Regarding the credit card debt, that one is kind of a mystery to me. While I have used credit cards to fund medical care I couldn’t fully pay for with my emergency fund, I rarely use them otherwise. It seems to me that it is essential to get this high-interest debt under control immediately. (If this is a problem for you, check out this article about paying down debt fast.

Spending on non-essentials seems to be a problem too. A lot of folks think that being on a budget means you can never have any fun, you can’t travel, you can’t go out to eat. So instead of creating a budget, they throw caution to the wind, spend while they have money, and complain when they don’t. I’d never say that you cannot travel, dine out, or do fun things. I do all of these and on a fairly tight budget. But I work it into my budget, I fund it with cash, and this comes after savings and all my other bills.

The biggest concern I see is that the money we Gen X-ers are paying into social security right now is going to fund the retirements of the Baby Boomers. The social security system is at a near-breaking point right now and most folks believe it may not even be there by the time we get to retirement age, much less for millennials. All that money that has been taking from our paychecks our entire working life…and none left when we need it. And if you think times are tight now, just wait until you’re too old to work and there’s no social security.

What do you think about this study?

Do you agree with this study that says Gen X is the generation is the one in the most financial trouble? Why do you think that is? Share your thoughts in the comments below.

25 Responses

Good article as always Daisy. The only thing that annoys me is when people refer to the Greatest Generation as the Silent Generation. One college professor said they just silently went along with whatever the government asked them… meanwhile they fought bravely in the Second World War and made so many sacrifices for our nation. God bless the Greatest Generation!

Silent Generation is after Greatest generation. They served in Korean war, not WW2. They unquestioningly lived with institutions founded by Greatest Generation. Read “The Fourth Turning” on such things: a REALLY fascinating book that is totally prophetic with regards to this present decade (written 1980).

I’m Gen-X.

Made some financial mistakes in the past but learned from them.

I have no CC debt.

Make like 95% of meals at home.

We put 18% of paychecks into savings/retirement.

Dine out maybe 2 or 3 times a month.

We do budget for those times we dine out, so it is not a surprise, or an expense we have to use a CC for.

We do budget in for vacations.

We sit down and ask ourselves what do we NEED to get done/purchase for the house for the year. Then, after everything else is paid off, money into savings, what is leftover is for WANTs. But NEEDs get addressed first.

Good for you, JarHead! I also have made some financial blunders, but I think the biggest thing is to recognize them, correct them, and not try to blame your financial position on the year you were born, the extravagance of our government, etc. Smart people don’t rush out to get the newest iPhone, smart TV, flashy car, watch, purse, whatever, just because society says they need it. (I’m an Army vet myself, thanks for your service.)

Check this in 20-30 years and it will just shift. The silent will drop off and the boomers will decrease as will Gen X then it will be the Millennials in “trouble” cause moms basement is gone and they gotta pay their way and their kids way LOL

I see I’m doing pretty good though especially in retirement savings. Heck I know that just from visiting with my friends though.

You can’t teach your children what you don’t know. I sometimes lament that my parents didn’t teach me most of the things I have learned are important over the last 70 years. But, in all honesty they didn’t know in the 1950’s and 1960’s when I was growing up what would be best for me in my 40’s, 50’s and 60’s. Why, because they were still in their 20’s and 30’s! My parents grew up during the depression, very simple times. Every decade that passes life becomes more complicated, so learn the basics of right behavior and stick with that.

The best we can do is to teach our children how not to destroy their own lives. Don’t get addicted (drugs, alcohol, food, sex, spending money, gambling, etc). How to work hard and not get distracted by unimportant, frivolous things (ignore the Jones). How to stay focused on the road when driving (road, traffic and pedestrian opsec). How to count every penny (yes Daisy, learn how to cook from scratch).

Probably most important is to figure out who can be trusted and who can’t. I still don’t know the answer to that except to say don’t pass on any secrets, especially your own! And keep your eyes open to who gossips, tells other’s secrets, lies and doesn’t live up to their promises. Most important, always make the other guy pay you in cash!

Social Security going broke gets a lot of attention, as it should, though the insolvency and financial devastation produced by Medicare and Medicaid is actually a much greater problem for younger and middle-aged people working today.

Yes I believe Gen x is in serious financial trouble. I am Kinda on the cusp between Gen x and millennials. Gen X is the first generation as a whole to DO WORSE THEN THEIR PARENTS. Boomers took most of the high paying upper jobs and held onto them longer(some working into their 70’s almost unheard of prior generations outside farmers maybe) than the boomer generation. The millennials will be the ones to benefit from the retiring boomer generation potentially the most. The trend of each subsequent generation doing worse than their parents is continuing and troubling. Plus our boomer parents had great benefits plans and pension plans. Current pensions plans are rarer and MUCH MUCH LESS BENBEFICIAL. boomers largely had defined benefit plans guaranteeing XX income in retirement, these have largely switched to defined contribution plans(AKA no benefit guarantees at the back end when you NEED the money) often they have disappeared altogether. We have a more fragile safety net than our boomer parents and it may not survive into our adult lives. Gen X unlike millennials and later grew up and started work under the assumption that there was a security network, where as millennials and later don’t believe the security net will be there and count on it less. With crushing national debt and world moving away from the petro dollar and rampant inflation we may be in real trouble in 10-30 years when we start to retire. Millennials have some protection in that they are not under the shadow of the boomer generation as much. Just my two cents worth…

I’m a “boomer” by definition, but being born at the tail end of that long span of years, most of what you described above regarding boomers really doesn’t apply to me. I did realize at a relatively young age that our government “management” of the social security system was a joke, and that depending on SS and the government wasn’t going to turn out well. There are those of every generation who plan for the future, and also those in every generation who live for today, damn the torpedoes. I believe that personal responsibility and awareness dictate your future security far more than the year you were born does.

Not to split hairs – but the generation dates seemed a bit off to us. While there is much argument about what years Generation X and Millennials were – I think it’s safe to adjust the date for both from 1977 to 1981.

The Boomer group should really be broken into two groups. I’m at the tail end of the “Boomer” group, my slightly younger brother is a Gen Xer. I’m basically in the same boat regarding social security. I paid attention, though, and prepared as if SS isn’t going to be there. My basic philosophy is to avoid depending on the government, because it has become the definition of incompetence and malfeasance.

o, the defined benefit pension! wasn’t around long, but great for those who got it. there are still some available in fed, state, and local governments and in some school districts. my personal experience with same is the gov’ts pay less than private industry, but have good benefits and usually pensions.

remember also that social security dates to the fdr era. didn’t have that before. my granny broke up housekeeping after grandpa died and took turns living with her 3 living children. she slept on a folding rollout cot in our dining room for 4 months of every year until she had to use a wheelchair and had to move into a “home”. think about that! it will help you save for retirement to avoid a meager end-of-life.

Your last paragraph that concludes out of the blue that SS won’t be there for the future is mistaken. What I have read on the subject concludes that there is plenty of money to fund future retirees. The main problem is that the high income earners right now pay up to a level that must be raised. I’m sure, and I know when I was in that rate in the past, that it’s really nice to get that bonus not paying SS half way through the year! But it’s not fair. High income earners can afford to keep on paying their SS insurance just like everyone else has to do. Besides, they get more when they retire! Also, the average age of death isn’t 65 anymore. It’s quite a bit higher, even though my own parents died at age 63 and 65. The average age for retirement hasn’t changed in a long time and it should, for actuarial reasons, be raised a couple of years. The money in SS has been “borrowed” by our own solid government into Treasury bonds for safety. It’s there and it will be there for you.

Why should people pay more FICA if they don’t get more?

One thing these types of studies never take into consideration is the amount of savings by past generations will never compete with the dollar value of the way we live now. In 1960, if you retired, (my grandparents age)and had managed to stash away a hefty 150,000.00- which would have been a lot, as each decade went by that money would be worth less and less. So if you are saving 18% of your current wages or 3 times your annual salary by age 40, just how much will that buy you in 2050. My guess is -not much.

I think that the money you are putting into Social Security may fund some of the earlier Baby Boomers, but realistically it’s a big black hole from which politicians feel free to suck funds for their pet projects. Personally, as one of the later Baby Boomers, I don’t expect to recoup any of the money I’ve paid in; it will be bankrupt by the time I’m allowed to try to draw from it if I live that long (the age keeps getting pushed out).

As the housing and construction industry is the driving force of the American economy the Baby Boomer’s greed for easy money by flipping houses mucked up the future of their grandchildren in that housing is expensive nowadays because of that.

Even to rent a modest apartment today takes at least four people living together.

Back in the 1990s flipping a house made an easy $17,000 or more profit per turnover increasing the cost of the building out of what people could afford and in effect mortgaging the future of following generations.

Greed.

While it is no excuse for cc debt, gen x was always sort of a “cursed” generation. When we entered the job market there were no jobs. When we finally got jobs 9/11 happened and the economy tanked along with our retirement funds. The dot coms crashed and oops, we were unemployed again. We pull ourselves up by our boot straps and get it together yet again, try to start families and buy houses but as soon as we do the real estate bubble bursts and we are upside down in our mortgages. The roller coaster continues with the 2008 recession and just when things are looking up our kids go to college and our parents get older and everyone is depending on us. We never really had a chance to build wealth. We just had really bad timing. Like I said before this isn’t an excuse for bad decisions but it does somewhat explain our pathetic retirement funds.

“Early-Boomer” here..born 3 days b4 D-day and retired in 2015. Folks today have had the basis of economics “educated away”.,. Here is Econ `101 from MY bygone days in college:

Lesson #1: There IS NO FREE LUNCH & No gvoernment money..it ALL must be stolen from working schlubs like me.

Lesson #2: In 1963 I was a Sophomore in college at a state Univ in the South, [incl 4 yrs mandatory ROTC], WORKING MY WAY THRU, W NO LOANS, as it were, w 4-5 different part time jobs [during my 4 years]….averaging about $1.75 per hour. Back then BS and BA degrees were earned in FOUR years 90+% of the time…and college loans were very RARE indeed.

Lesson #3: : The ‘federal minimum wage’ (FMW) back then was ‘only’ $1.25 an hour, which sounds crappy does it not? But…. wait..that was FIVE 1963 quarters per hour… {90% SILVER quarters} back then, before DEMOCRAT Lyndon Johnson signed the bill removing the silver from the coins and recalling all paper “US silver certificates”…in 1965..

Lesson #4 Yes up til 1963 you could take a paper “$1 silver certificate” to any bank in 1963 and the nice banker wd trade to you a US uuuge $1 silver dollar coin for that certificate, bks that piece of paper said… “pay to the bearer on demand one dollar silver” . right on it. .

FF to 2019..IF you still had those 5 1963 quarters [OR a $1 silver certificate” plus one 1963 Quarter].., (you DO have some, right? I do)…you could take them to any coin shoppe and the nice man there wd TRADE to you about 17-18 paper “Federal Reserve notes” for those 5 silver coins.or the $1certificate plus a 1963 quarter.

Lesson #5: The paper Federeal Reserve Note does not promise to pay you $1 silver., but in fact it now takes about 20 $1 ‘federal reserve notes’ to “buy” even a junk well-circulated silver dollar coin.

Lesson #6. So, the libs today want a FMW of $15 huh? LOL on us bks THAT is less in buying power than the MW back in 1963.

BTW..I well remember that a new V8 Corvette cost about $3500 back in 1963

According to Alan Greenspan, “There will always be Social Security. The question is what will it buy?”

I agree with this and have been referring to it as “Socialist Insecurity” for years now. :)))

This article is excellent and, as always informative. I must say, however, that much of what is spoken as current could just as well been written in the late 1080’s and early 1990’s. The Boomers were reading the same back then, only they were the “in-between generation” at the time.

The biggest difference for which we should all lament, is that inflation has killed off the dollar’s value to the point that now it is almost impossible for younger people to get an affordable advanced education, or afford a mortgage. So, who would not understand the prevalent Gen. X attitude: “just throw it to the wind, and enjoy it while you can.”

Inflation: Hidden Tax: Gold Standard ends on August 15, 1972

“In 1971, President Richard Nixon declared that U.S. dollars could no longer be converted into gold, whether by foreigners or by U.S. citizens.”.

Note the phase the “… U.S. dollars could no longer be converted into gold, whether by foreigners …”

Because of the North Vietnamese getting massive amounts dollars from the U.S. military during Vietnam for drugs, prostitution and other means from the U.S. soldiers, if they would have cashed in the dollars for gold we would have been bankrupt.

Another name for the Vietnam War was the “Children’s Crusade” since most of the draftees were eighteen years old or close.

Baby Boomers: Born 1946 – 1964. 1946 + 18 = 1964

The Vietnam War ran from 1955 to 1975. President Johnson escalation of the war was from 1963 -1969. The war was still hot to 1975.

Boomers

L. Frank M Baum’s “Wizard of Oz” published in 1900.

https://en.wikipedia.org/wiki/Political_interpretations_of_The_Wonderful_Wizard_of_Oz

Hugh Rockoff suggested in 1990 that the novel was an allegory about the demonetization of silver in 1873, whereby “the cyclone that carried Dorothy to the Land of Oz represents the economic and political upheaval, the yellow brick road stands for the gold standard, and the silver shoes Dorothy inherits from the Wicked Witch of the East represents the pro-silver movement.

Pink Floyd’s album “Dark Side of the Moon: released in 1973.

“Dark Side of the Rainbow – also known as Dark Side of Oz or The Wizard of Floyd – refers to the pairing of the 1973 Pink Floyd album The Dark Side of the Moon with the visual portion of the 1939 film The Wizard of Oz”.

Those Boomers again.

not

Tongue-in cheek history.

… er, continued.

According to Strauss & Howe’s fourth generation theory or the “Four Turnings”, “The Wizard of Oz” was published in 1900 during the Lost Generation, the Boomers of that time.

It then leapfrogged in 1939 when it was made into a movie during the fourth generational “Silent Generation” (Artists) to land or be picked up by the twenty century Boomer Roger Waters and be rediscovered later during the Millennial’s time span when it was synchonized to the novel.

Maybe the Centennials/Artists will adapt it into something.

nah

Carl Jung Redux.

Know why so many Xers have financial problems? Because it seems as if many Boomers achieved success then drew up the ladder after them. It’s a generalization obviously so not true for all, but was true in many cases. They are also living longer than most Xers hope to, and had better medical care than many of us did.

Also, I will continue to call the generation who fought world war 2 “The Greatest Generation” and don’t hold with this newfangled “silent generation” stuff.

Great article, Daisy, and a thought provoking one. I must say though, that I don’t eat out at restaurants, and I have maybe purchased $3 in lottery tickets in my life time. I do have credit card debt but that has more to do with no relatives wanting to give me a loan when unexpected financial disasters struck – financial disasters that nearly always outstripped what little savings I had. Why didn’t I save more? Well, I own my car, I have basic liability insurance, I don’t pay for cable TV, and I have a $50 phone bill for two people, but I also have medical bills and couldn’t get a decent job till just over 2 years ago, again because most opportunities in my field were sewn up and I didn’t start making a good living till I was 38.

I’m not playing a blame game here, just making it known that high debt has a lot of factors and it’s not always because a person is foolish. (I know you aren’t saying that Daisy but a lot of people do.)

Each generation has seen that the older generations pull up the ladder after they started in work.

When my grandparents attended college, born about 1890, many people didn’t even graduate high school. About all that was required was a high school diploma and a desire to attend college. Part-time work was enough to pay university tuition and living expenses. All four of my grandparents graduated, two to get master’s degrees.

When my parents, born in the 1920s, attended university, my father benefited from GI bill, even so he needed part-time work and to borrow some from his parents. But he was able to get into grad school with a C average. He finally was “urged” into retirement at 78, still at the cutting edge of his field.

I’m a boomer, and it took me eight years to graduate—go to school a year, work and save a year or two, go to school a year, work part-time while taking classes, and I graduated without student debt. But when I looked at grad school, the requirement was an A average, which I didn’t have because of spending so much time working to pay for university. That ladder had been pulled up.

I’ve had to live very frugally with low income. I’ve made some mistakes which cut into my income, so I’ve ended up with no property and virtually no savings, but at the same time no debt.

My children are millenniels. Two of them were able to get their first two years of undergrad studies free tuition because of a program unique to their situations. All three went into STEM fields with high demand, therefore good salaries, so have been able to pay off their student loans. Their student loans were far less than many of their fellow students, because they had learned to live frugally while at home.

The reason I tell this story is to show that each generation has seen ladders pulled up in front of them. My sons benefited in that they like working in fields that didn’t exist or were in their infancy when I graduated. The ladders that are being pulled up are costs for education, education requirements for jobs where the education isn’t really needed, higher barriers to get an education, red tape and licensing requirements for jobs that don’t need them, lower wages vis-à-vis living costs, older generations staying at their jobs longer before retiring, therefore restricting opportunities for the younger generations, and so forth.

I now tell young people not to bother with college, unless they have rich parents who will pay for them, or that the career they intend requires college, like engineering. Make sure they know the 3 Rs and they can work at most jobs. The 3 Rs should be mastered by eighth grade. A few jobs may require trade school, which usually can be completed in a year or two, or even as part of an apprenticeship that can pay to go to school. I benefited from finishing my degree, but not financially and I could have gotten the same benefits outside of classroom participation.

Unfortunately, the latest ladder being pulled up is a decent grade school education. Kids are “graduating” high school unable to do the things expected of me by fourth grade. Without a mastery of the 3 Rs, the next generation are really restricted in what they can do. This is the cruelest ladder pull up of them all.